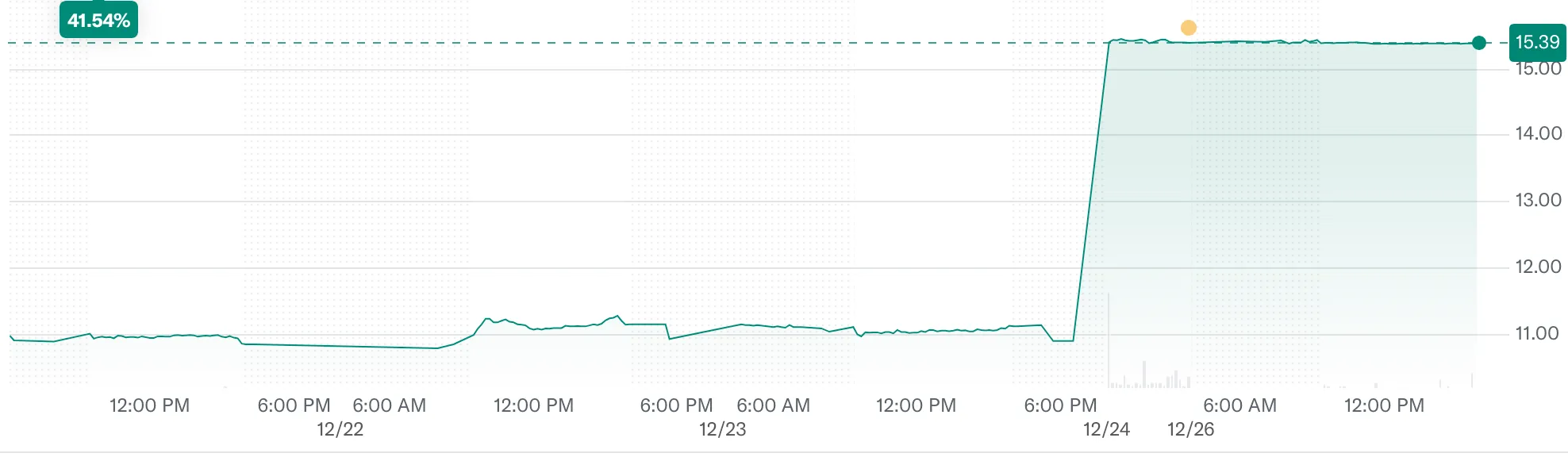

Earlier this week, Sanofi (NASDAQ: SNY) announced that it was acquiring Dynavax Technologies (NASDAQ: DVAX) in an all-cash transaction valued at approximately $2.2 billion. That’s a 39% premium over its pre-announcement price.

Here’s how the market reacted …

To be sure, this wasn’t just another run-of-the-mill M&A headline. It represents a strategic extension of Sanofi’s immunization footprint and could be a compounder story across both vaccine markets and long-term healthcare portfolios.

You see, Sanofi didn’t just buy Dynavax for the sake of acquisition statistics. The French pharma giant is buying Heplisav-B, Dynavax’s approved adult hepatitis B vaccine, a two-dose, one-month regimen that outcompetes traditional three-dose schedules.

Nearly 100 million U.S. adults born before 1991 remain unvaccinated against Hepatitis B, representing an additional addressable population.

Sanofi also gained access to Z-1018, a shingles vaccine candidate in Phase 1/2 development that’s generating early clinical data and could effectively compete with incumbents.

Understand, shingles isn’t a niche concern. Roughly 1 in 3 adults will experience it in their lifetime, and just a small handful of players dominate the current market.

Dynavax’s Z-1018 candidate is still early-stage, but it’s backed by promising Phase 1/2 data and differentiating adjuvant technology. If this program can match, or even slightly erode, the market share of established leaders, the revenue run-rate could grow substantially over time.

This unmet need for additional treatment options for Hepatitis B and shingles underpins the strategic rationale for Sanofi’s move. Investors increasingly appreciate businesses that align public health impact with revenue growth – and this transaction checks that box.

Still, $2.2 billion isn’t pocket change, so let’s take a closer look at the deal valuation.

The Baseline: Price Paid vs. Current Revenue

Sanofi is acquiring:

- A marketed adult hepatitis B vaccine that’s already generating meaningful sales, and

- A phase 1/2 shingles vaccine candidate with promising early data and the potential to compete with entrenched players.

To put some numbers on this, Hepislav-B reported third-quarter 2025 revenue of about $90 million, and Dynavax expects roughly $315 million to $325 million in full-year 2025 net revenue from this vaccine.

Sanofi paid $2.2 billion for Dynavax, roughly 6.7 times the company’s projected 2025 revenue excluding growth. That multiple isn’t cheap, but in vaccines – especially commercial brands with differentiated features – it’s not unreasonable. Indeed, it’s far below the multiples we see in high-growth biotech, where pipeline value dominates valuation, yet it preserves current revenues while buying future optionality.

Overall, the valuation makes sense.

Sanofi’s $2.2 billion valuation for Dynavax boils down to:

📌 A stable revenue base (~$315–$325M projected Hepslisav-B sales in 2025)

📌 Plus optional growth from an early shingles vaccine with blockbuster potential

📌 At a multiple that respects both current performance and future promise

In short: Sanofi didn’t overpay for hope, it paid for revenue today with optionality built in for tomorrow. For investors aligned with long-dated growth themes in healthcare – especially vaccines – that’s the kind of disciplined valuation decision that can drive outsized returns over time.

Publication Date

December 26, 2025

Category

Healthcare / Biotech

Jeff Siegel

Senior Content Contributor