Big news today for Organon & Co. (NYSE: OGN) today.

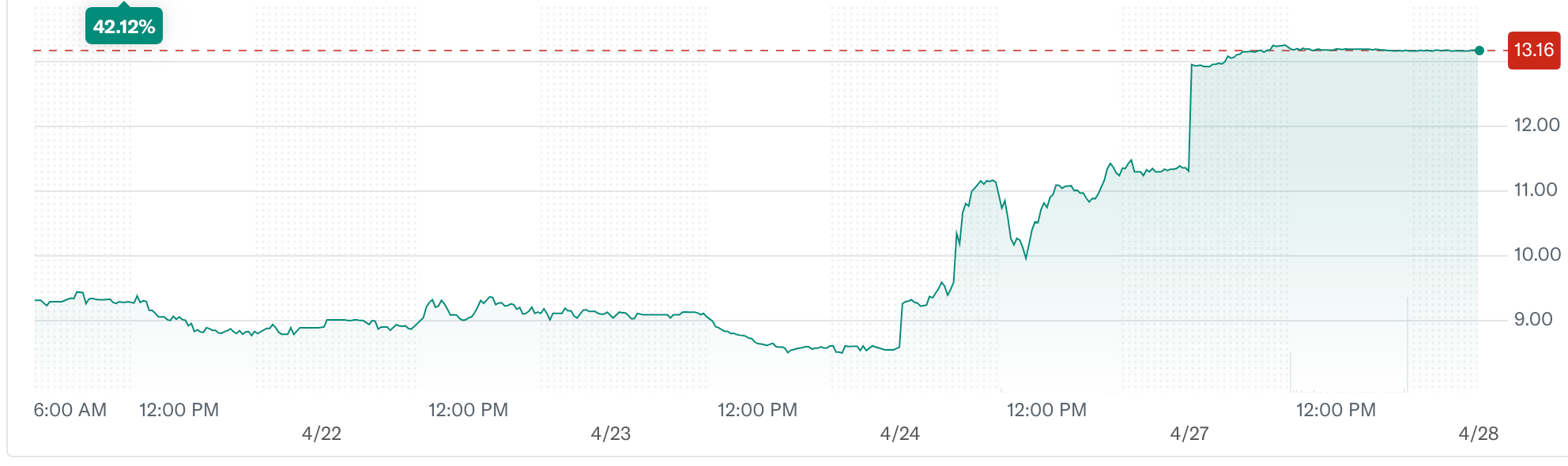

Shareholders were treated to the news that the company was being acquired by Sun Pharmaceutical Industries in an all-cash deal valued at approximately $11.75 billion, including debt. That makes it the largest overseas acquisition ever completed by an Indian drugmaker.

With this acquisition in place, Organon brings roughly $6.2 billion in annual revenue, a portfolio of more than 70 established medicines, and distribution across 140 countries.

Essentially, Sun’s revenue base nearly doubles now while its geographic exposure expands beyond its current concentration.

And of course, Organon shareholders pocket a nice little profit.

Generic obstacles

If you’re unfamiliar, Sun Pharma has historically been tied to generic drugs, particularly in the U.S. market. That segment has become increasingly difficult.

Pricing pressure has intensified. Regulatory complexity has increased. Margins have compressed. This deal is a response to that environment.

To be sure, Organon is not a high-growth biotech company. It’s a portfolio of established, cash-generating products, particularly in women’s health, biosimilars, and general medicine. These are not breakthrough therapies, but they are durable revenue streams.

What Sun Gets

The acquisition gives Sun three things immediately …

First, scale in women’s health.

Organon’s portfolio includes products like contraceptives and fertility treatments, positioning the combined company among the larger global players in that segment.

Second, global reach. Organon operates in markets where Sun has historically had limited presence, including parts of Latin America and Asia.

Third, cash flow. Organon’s business is built on established drugs with predictable demand. That provides a base that can support further expansion into specialty areas.

Put simply, this is a cash flow acquisition.

Bottom line: Sun Pharma has made a calculated shift.

It’s trading a portion of its balance sheet for:

- established revenue

- global distribution

- and exposure to higher-margin segments

If integration proves to be smooth and cash flows hold, the company emerges as a more diversified global player. If not, it becomes a larger company with more complexity and more debt.

Only time will tell.

Publication Date

April 27, 2026

Category

Healthcare / Biotech

Jeff Siegel

Senior Content Contributor