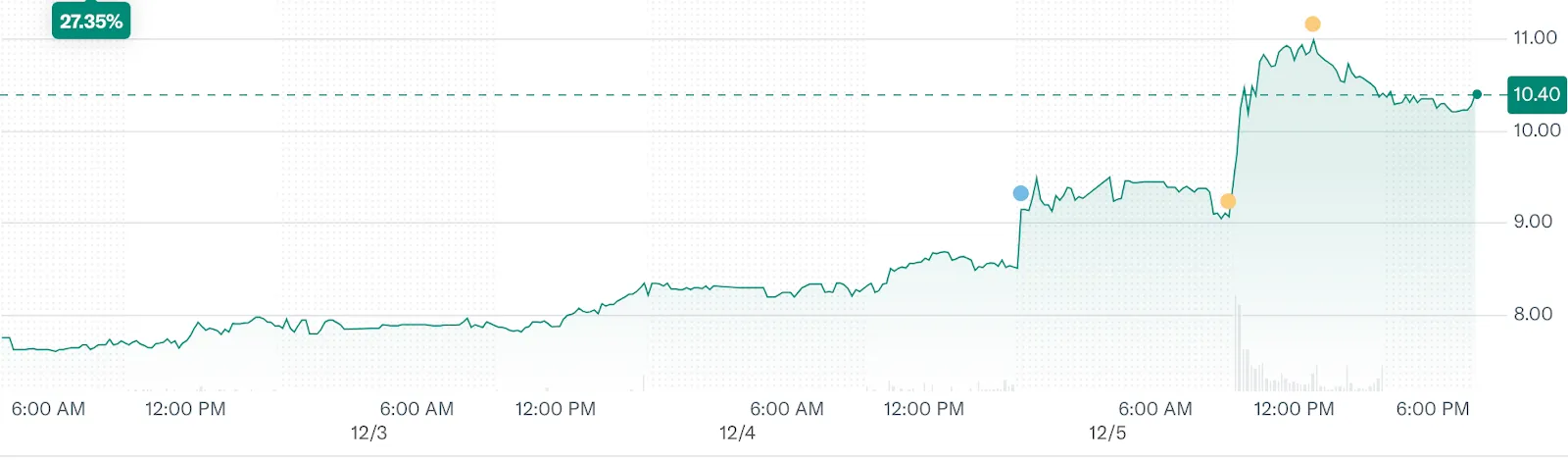

ChargePoint (NYSE: CHPT) surged yesterday after releasing solid Q3 results and upbeat guidance.

For Q3, ChargePoint delivered $105.7 million in revenue, representing an increase of about 6%. This topped Wall Street’s expectations.

Gross margins also improved significantly, and management projected next-quarter revenue around $105 million at the midpoint, which is above consensus.

The company was able to push adjusted gross margin to ~33% (vs prior weaker quarters) and announced it cut about $172 million of debt. That reduction in debt load certainly bolstered investor confidence.

We also saw some signs of strategic discipline. Growth in its higher-margin subscription business (up ~15% YoY), better product execution, and early adoption of next-gen hardware/software, all suggested ChargePoint may be shifting from a high-burn startup toward a more stable business model.

For a company that’s been taking it on the chin this year (share price down considerably, business headwinds, investor skepticism), this quarter’s combination of revenue growth + margin improvement + debt reduction is exactly what you want to see to turn sentiment.

In a sector where many peers still burn cash and post losses, ChargePoint’s tightening of the belt and clearer path to stability makes it stand out.

Of course, we can’t lose sight of the fact that losses remain sizable. The company still isn’t profitable, adjusted EBITDA remains negative, and free cash flow is still negative.

Macro headwinds linger, too, with EV adoption growth in the U.S. being uneven, government incentives disappearing, and competition in charging infrastructure heating up. This means execution still matters – a lot.

Truth is, this rally might be partly driven by short-term sentiment, not long-term confidence. For ChargePoint to truly survive (let alone thrive), it needs sustained margin improvement, better cash flow, and ideally a clearer path to profitability.

If ChargePoint can stay lean, improve margins, and continue to grow revenue (even slightly) for the next three years, it could be in an excellent position to thrive in a post-Trump world.

To be sure, no one wants to own a stock whose success is heavily tied to policy. But the long-term view for EV adoption remains strong - on a global scale. The U.S. is now turning into a laggard, but as costs continue to fall and range continues to improve, this could change, even without policy support. This is definitely the direction in which we’re heading, too.

ChargePoint is in an excellent position to capitalize on this truism, as long as it can weather the storm of a very vocal anti-EV administration and tariff pressures.

If ChargePoint does deliver positive results again next quarter, expect to see even more investor confidence.

Publication Date

December 6, 2025

Category

Energy

Jeff Siegel

Senior Content Contributor

.webp)