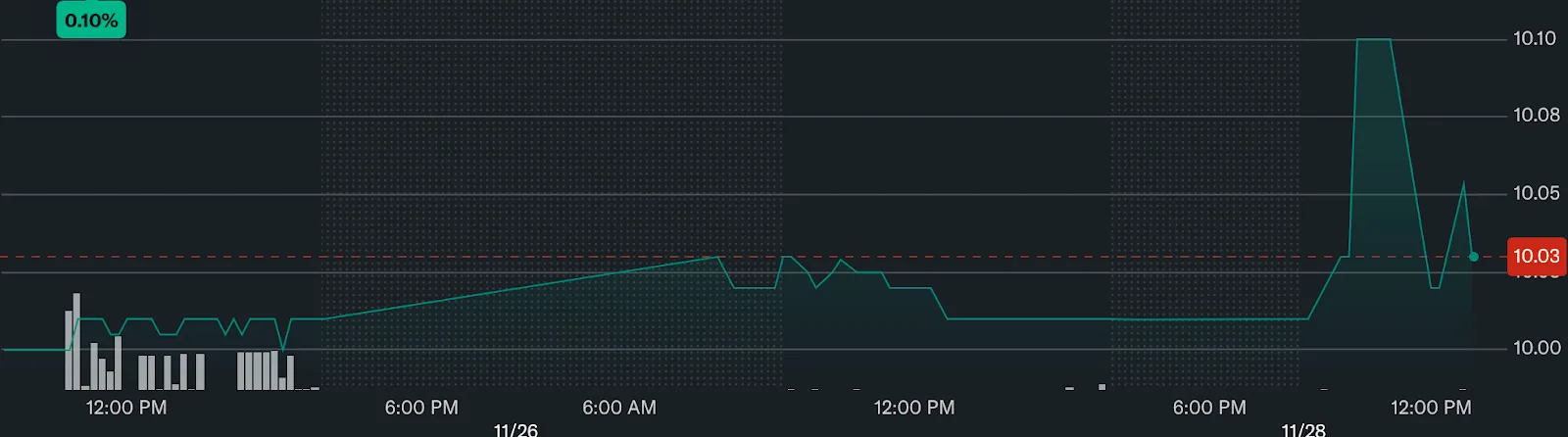

There wasn’t much enthusiasm for the Invest Green Acquisition Corporation (NASDAQ: IGACU) IPO.

To be honest, I don’t think it was well-promoted, which could be a good thing. Too much stock promotion typically stinks of pumps, dumps, and general shady behavior. That being said, because I have a history of creating significant wealth in what’s often considered “green” sectors, the name piqued my interest.

Could this be an under-the-radar play on something that could allow us to do well by doing good?

Let’s take a closer look.

At its core, Invest Green offers investors entry into a “green deal pipeline.” Not a single business, but potential access to several high-growth targets that are (or could be) driving the global energy transition.

This particular SPAC is being positioned to capitalize on megatrends: climate policy, rising demand for clean power, nuclear innovation, sustainable finance, and the general shift away from fossil fuels.

In theory, this sounds appealing, but in practice? Well, we haven’t seen “in practice” just yet. Thus, the problem with SPACs sometimes: big promises, no execution. Not that this is the case with Invest Green, but we just don’t know yet. So let’s focus on what we do know.

Capital Raised, War Chest Ready

With $172.5 million in the till, Invest Green has plenty of dry powder to build something worthwhile. And the plan is quite simple:

- Go after mid-sized renewable or nuclear developers (solar farms, wind, hydro, small modular reactors)

- Consolidate smaller “green infrastructure assets.”

- Invest in technologies supporting the energy transition (storage, grid software, sustainable finance platforms)

The company has the cash to wet its beak on all of this. So let’s take a look at some of the upsides here.

4 Pillars of Success

Here are four avenues Invest Green can take to build a successful business that rewards shareholders.

- Acquire a high-growth renewable energy platform, such as a solar/wind/energy-storage operator. Particularly one with long-term contracts or stable cash flows, such as Array Technologies (NASDAQ: ARRY), Emeren Group (NYSE: SOL), or PowerBank (NASDAQ: SUUN).

- Buy or merge with a next-gen energy tech firm: e.g., battery storage, grid-stabilization software, energy-as-a-service providers, or “nuclear-adjacent” infrastructure.

- Enable consolidation in fragmented green industries: Many renewable energy developers remain small and under-capitalized; a well-capitalized SPAC could roll up multiple assets, bringing scale and efficiency.

- Ride policy and ESG tailwinds, especially if governments increase subsidies or regulations favoring clean energy.

Still, there are risks.

First, there’s just no guarantee on any of this. As with all SPACs, until a deal is announced, investors don’t actually own a real operating company.

Also consider “green” market cyclicality. If interest in “green” fades or commodity/energy markets shift, valuations could compress quickly. To be fair, I really don’t see this happening, as it’s not really about “green” anymore. It’s just about affordable megawatts. And solar and wind have already won that race.

And if you’re not into something like this for the long haul, consider that clean energy infrastructure is typically geared for long-term gains, not short-term wins. So if you’re looking for a quick score, this isn’t it.

If you’re a regular reader of these pages, you know I’m quite skeptical of most SPACs. But I will watch this one carefully. Not because it’s guaranteed to skyrocket, but because it’s offering a ticket to a thematic megatrend waiting for consolidation and capital.

Of course, the company just went public, so for now, let’s not make any sudden moves, but also keep this one on our “watch list.”

Publication Date

November 28, 2025

Category

SPACs

Jeff Siegel

Senior Content Contributor

.webp)